.svg)

The story starts in Egypt, in 1963.

Ahmed Elnaggar opened the Mit Ghamr Savings Bank in a small Delta town, offering interest-free accounts to farmers and merchants who had stayed out of formal banking on religious grounds. There were no shareholders demanding returns. Deposits were pooled, invested in local businesses, and profits were shared. The model was simple, trusted, and deeply local.

Mit Ghamr lasted only four years before political pressure shut it down. But the idea held. Dubai Islamic Bank opened in 1975 as the first fully commercial bank operating under Shariah principles. From there, the sector grew steadily across Malaysia, Bahrain, Pakistan, the UK, and Indonesia, building a separate financial ecosystem alongside its conventional counterpart.

Today that ecosystem manages an estimated USD 5.47 trillion in assets globally and is growing at roughly 11% a year. The institutions are no longer small or local. They are multinational, digitally active, and competing for the same customers as any other retail or wholesale bank.

But the infrastructure behind them has not kept pace.

The idea is old. The engineering is not.

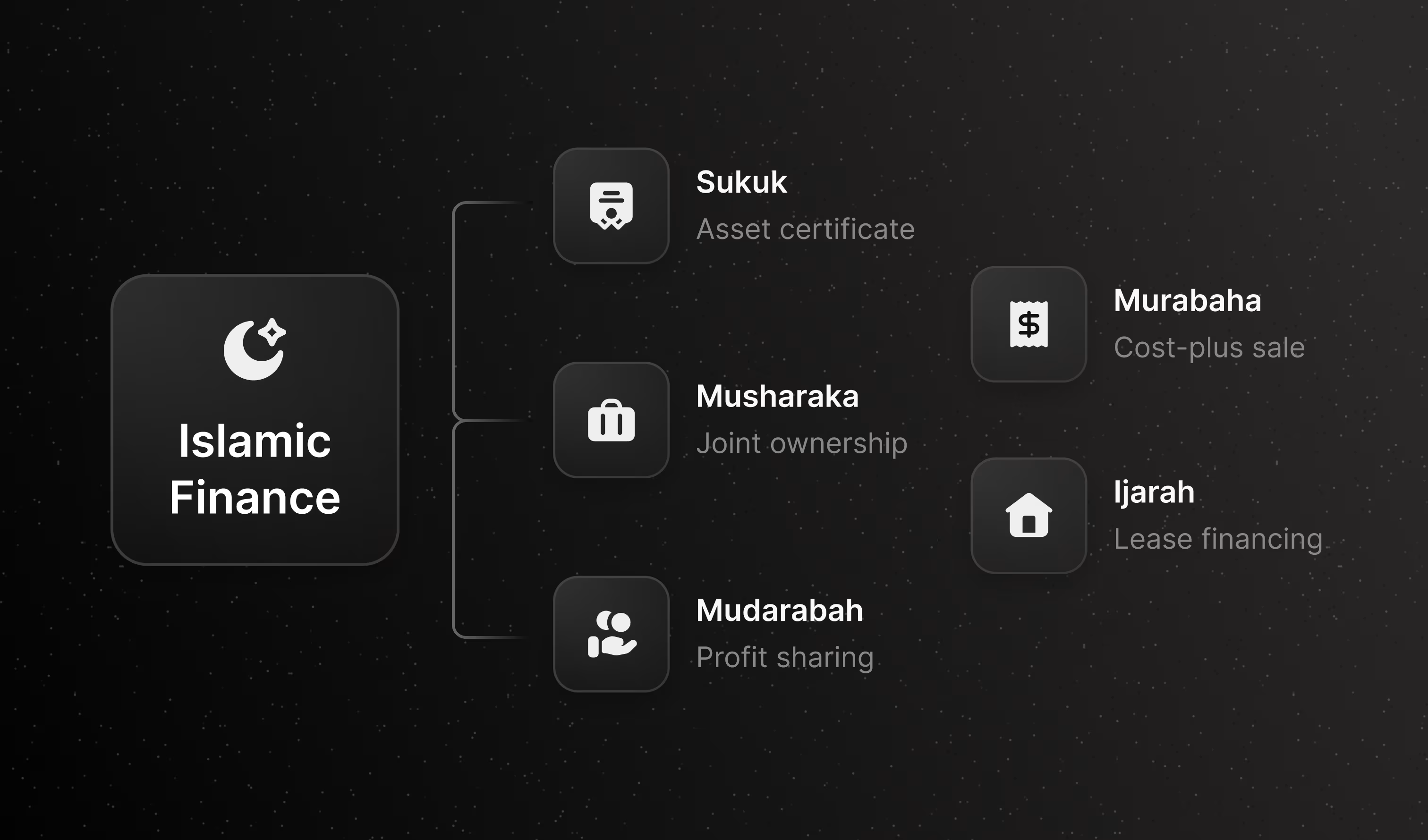

Islamic finance is not complicated in principle. It is a set of contractual frameworks designed to replace interest, known as riba, with profit-sharing, asset-backed transactions, and fee-for-service structures. A murabaha is a cost-plus sale, not a loan. An ijara is a lease that transfers economic use without transferring ownership. A musharaka is a partnership where both parties share in gain and in loss. Sukuk are instruments structured around ownership of a real asset rather than a debt obligation.

These frameworks have operated for centuries, and the prohibitions they encode are clear. What is not clear, and what makes modernising Islamic finance genuinely difficult, is how those structures are implemented in software, operationalised across borders, verified by Shariah supervisory boards, and delivered to customers who expect the same real-time experience they get from any other digital bank.

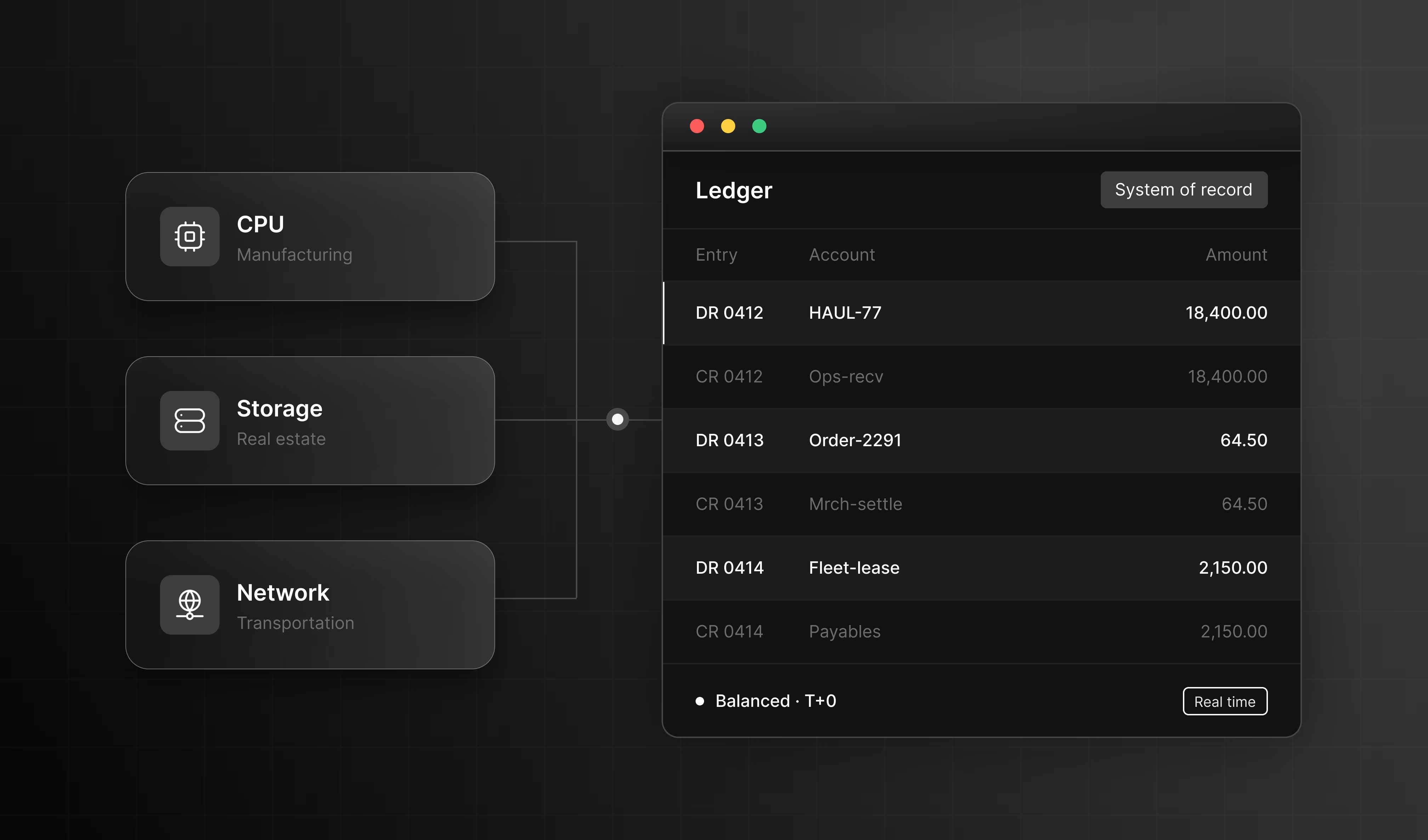

A conventional personal loan is a straightforward obligation: borrow, repay, with interest. An equivalent Islamic finance product, a diminishing musharaka or a tawarruq arrangement, requires the bank to record multiple contract legs, track the underlying asset, and attribute profit to the correct period at the correct rate, all while maintaining an audit trail that a Shariah board can inspect. The loan management architecture for one is nothing like the architecture for the other.

That gap is where the modernisation challenge lives.

The components that need rebuilding

Islamic finance institutions today are generally running one of three infrastructure configurations.

Legacy monolithic cores: Many banks across the GCC and South Asia have been running modified versions of conventional core banking systems with Islamic product modules bolted on. These systems were not designed for Shariah-compliant contract logic. Compliance checks are largely manual. Introducing a new product, such as a Shariah-compliant buy now, pay later offering or a structured savings account, requires Shariah board sign-off plus engineering work that can take months.

Purpose-built Islamic cores: A newer cohort of providers has built from the ground up for Islamic product logic.

Digital-native challengers: A third tier of companies is building financial products within the Islamic framework without being banks at all.

What connects all three tiers is that they depend on the same back-office capabilities: accurate ledgers that track multi-leg contract structures, deposit infrastructure that distributes profit rather than interest, and card-issuing systems that can enforce spending category restrictions required by Shariah supervisors. These are not trivial builds. And none of them can be handled well by infrastructure designed for a different contractual model.

The infrastructure problem

There is a structural tension at the centre of Islamic finance modernisation that conventional fintech does not face in the same form.

Shariah compliance is not a flag you set in a database. It is a continuous legal opinion, renewed by a board of qualified scholars, applied to specific product structures in specific jurisdictions. What counts as permissible in Malaysia may differ from what is permissible in Bahrain or Pakistan. A financial institution offering products across multiple markets is therefore managing multiple Shariah interpretations simultaneously, each requiring its own audit trail and supervisory sign-off.

This creates fragmentation at every layer. At the product layer, each variant of a murabaha or ijara must be separately reviewed and documented. At the technology layer, no single compliance engine exists that can automate Shariah supervision across jurisdictions, so institutions build bespoke systems that cannot communicate with each other. At the onboarding layer, customer-facing applications must collect documentation and consent specific to the contract type being offered, not just the standard KYC flow.

The deeper problem is that fragmentation compounds over time. A bank using one system for digital loan origination, another for profit distribution, and a third for payment routing ends up with reconciliation breaks, audit gaps, and Shariah supervisors who cannot get a clean view of the full contract lifecycle. The corrections and write-offs that result are rarely visible to the customer booking the product. They sit inside the operations team, absorbing time and cost that the market does not see.

What this looks like in practice

The institutions doing this well are treating Islamic compliance as a first-class design constraint, not an afterthought applied at the end of the build.

What most environments share, whether in Malaysia or in Bahrain, is a recognition that Islamic finance cannot modernise by placing digital interfaces onto unchanged back-office logic. The infrastructure must encode the contracts. Profit-sharing ratios, asset ownership schedules, ijara lease terms, and Shariah audit records all need to live in the core, not in spreadsheets or side systems maintained by operations teams.

The institutions that get there fastest tend to be those with modular, API-first infrastructure where each component, the ledger, the loan engine, the payments layer, can be updated or replaced without dismantling everything around it.

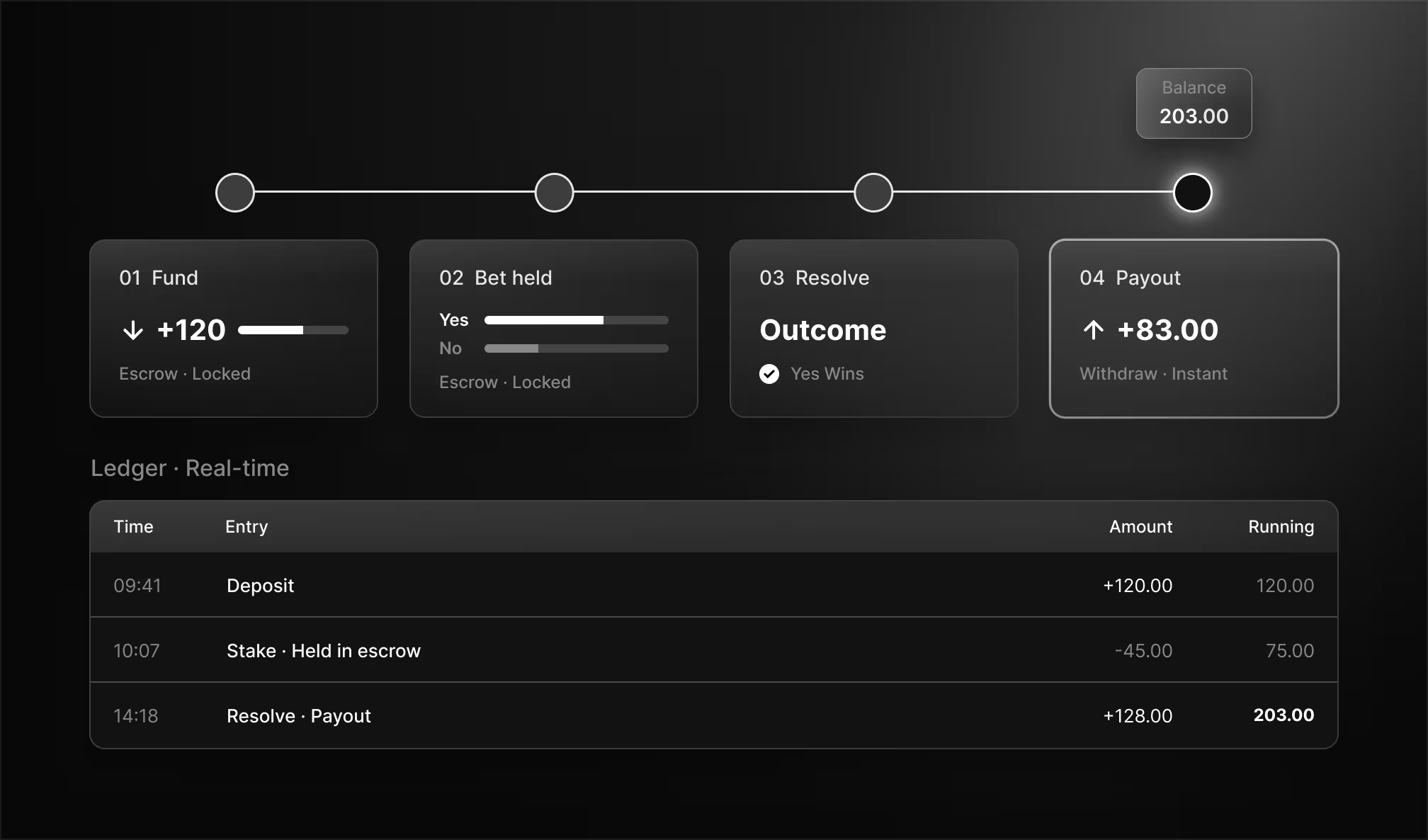

When Layla books a Shariah-compliant home financing product through her bank's mobile app in Kuala Lumpur, or Daniel invests in a sukuk through a digital brokerage in London, what they see is a clean interface and a clear profit schedule. What they do not see is the contract logic, the Shariah audit trail, the multi-leg ledger entries, and the compliance checks that made it possible.

That is what modern Islamic finance infrastructure is actually doing.

The market is large. The demand is real. The complexity is in the plumbing.