.svg)

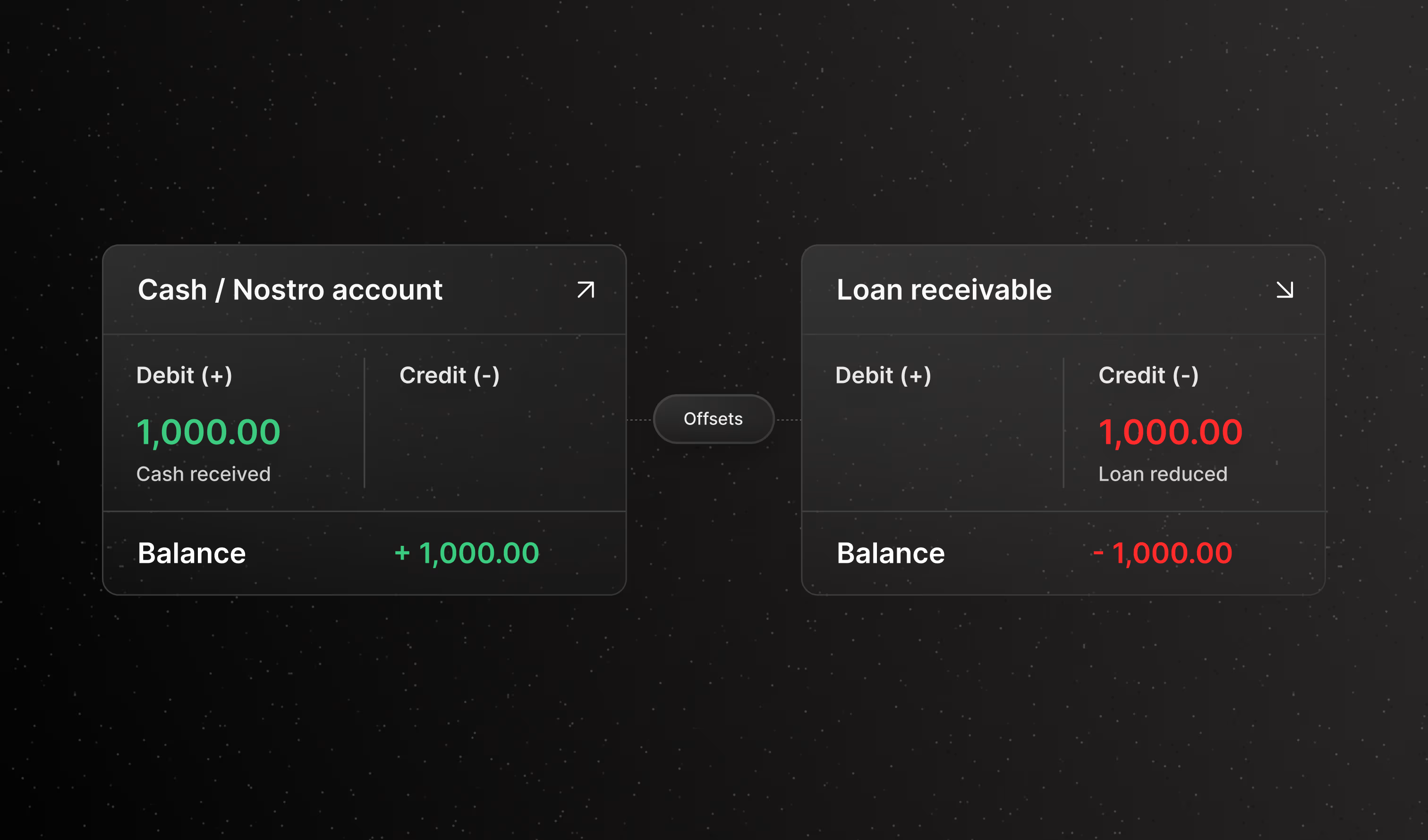

A customer taps a card for 200 riyals. In the half-second before the screen confirms it, a ledger somewhere has to do something exact: debit their account 200, credit the merchant's, and refuse the whole thing if those two numbers don't match to the halala. That matching rule is double-entry accounting, the centuries-old discipline where every credit has an equal debit, so the books always balance and any discrepancy surfaces the instant it appears.

Most people meet a ledger only as that afterthought, the silent layer below an experience that feels effortless. But the ledger is the record of every debit and credit an institution holds, and everything stacked on top inherits whatever state it's in. Get it right and the products above it move fast. Get it wrong and every balance, statement, and decision built on it carries the same error forward.

The trouble is that most institutions run a ledger that lags reality. Either they build a custom system, which is expensive and breaks in ways nobody catches until reconciliation, or they run general accounting software that was never designed for real-time, high-volume money movement. Both produce the same defect: a balance that's true at 2am and approximate by lunchtime. End-of-day batch jobs. Gaps that someone reconciles by hand the next morning.

What financial ledger software actually has to do

A ledger for financial products is not desktop accounting software with more rows. Sitting on the double-entry foundation, it has to hold four things at once that general tools were never asked to manage.

It has to update balances in real time, with no batch delay between money moving and the record reflecting it. It has to keep audit trails that are immutable and timestamped, so every entry is traceable and nobody can quietly rewrite history when a regulator asks. It has to handle multi-currency balances with conversion built in, because a wallet funded in riyals and a card settling in dollars belong to the same customer. And it has to be programmable, so an event like interest accrual or a fee posting writes its own balanced entry through an API instead of waiting for someone to key it in.

Financial ledger software built to those four demands changes what the layers above can do. When cards, wallets, loans, and deposits all post to the same ledger, reporting is unified and the reconciliation overhead between products disappears, because there's only one record to reconcile against: itself.

Why fragmentation is the real cost

Picture a bank launching a digital wallet. On paper it's an app, a ledger, and top-ups. In practice it's a chain of separate vendors: one supplies the core ledger, another issues the cards, a third handles identity checks, and each piece keeps its own version of the truth. Every integration is a separate contract, a separate data format, and a separate point where the numbers can drift apart.

The wallet the customer eventually opens is clean. The infrastructure carrying it is four systems taped together, reconciled against each other on a schedule rather than agreeing by design. The cost goes beyond the months lost to integration; the institution now owns a permanent reconciliation problem, and every new product it launches widens the distance between its records and what actually happened.

A single ledger underneath every product removes that distance. One source of truth means wallets, cards, lending, and deposits all draw their state from the same place, so a balance is a balance no matter which product is asking. The work that used to go into making four systems agree goes into building the next thing instead.

The AI part nobody can skip

Every institution now wants AI somewhere in the stack: underwriting that reads more than a credit score, fraud detection that catches patterns as they form, agents that answer a customer's questions about their own money. All of it depends on one thing that has nothing to do with the model itself. It depends on the data the model reads being correct, current, and complete.

The ledger is where that data lives, which makes it the constraint. A model underwriting a loan needs the borrower's real position right now, a fraud system needs to see the transaction as it posts. An agent quoting a balance to a customer cannot be working from yesterday's number. Feed any of them a record that lags reality and they produce answers that are confident and wrong, which in finance is worse than no answer at all.

The failure is mechanical. A model is only as good as its inputs, and inside a financial institution those inputs come from the system of record. A real-time, programmable, double-entry ledger with full audit trails hands a model clean inputs by construction: current balances, traceable history, no gaps to paper over. A fragmented stack of lagging records hands it noise and calls it data.

So the real question for an institution is whether the records underneath are good enough for AI to mean anything. That decision gets made long before the model does, in the choice of what keeps the books. Treat the ledger as the foundation and there's something solid to build on. Treat it as an afterthought and the next few years go to reconciling the mess instead of building on top of it.